Law firm accounting software like MyCase, offers law practice management and accounting features in a single package, so all critical accounting information is current, compliant, and audit-ready. With an all-contained law firm bookkeeping and accounting system, users can enjoy having all their financial data in one place—reducing the risk of critical errors. This gives you the best of both worlds while making your law firm’s comprehensive accounting situation easier to manage. Consider what you need, and seek out accounting software that fits those needs.

Improve your law firm’s cash flow

It’s the practice of keeping client funds given in trust, including unearned fees paid as a retainer, court fees, settlement funds, or advanced costs, in a separate account from law firm operating funds. By integrating these best practices into their operations, law firms can achieve a high level of financial management and operational efficiency. This proactive approach to law firm accounting not only supports compliance and enhances profitability but also contributes to the firm’s long-term sustainability and success. The distinction between legal accounting and general accounting lies in the nuanced understanding of legal regulations and the ethical considerations specific to the practice of law.

Why bookkeeping and accounting matter for law firms

For a CPA to work effectively, they will need you to provide accurate, up-to-date financial statements. Whether you’re good with numbers and spreadsheets or not, every lawyer needs to understand the basic role that bookkeeping plays in their business. Unless the IRS requires you to use the accrual method—for law firms, this rule only kicks in once you start making $10m a year—which method is best will depend on your accounting needs. Your business’s accounting method will affect cash flow, tax filing, and even how you do your bookkeeping. Granted, if your bookkeeper and accountant are on board with it, and you take care to flag transactions properly, using your business account for personal transactions (or vice versa) isn’t the end of the world. And when you commingle your personal and business finances, the following problems can arise.

Creating an Effective Accounting Client Onboarding Checklist

Generally Accepted Accounting Principles (GAAP) are common accounting rules, standards, and procedures developed by the Financial Accounting Standards Board (FASB). GAAP often serves as the foundation of the framework used by many law firms to help guide proper financial accounting and the preparation of financial statements. The overarching goal of GAAP is to ensure all companies, including law firms, consistently craft financial statements that are complete and comparable. The ability to journal entry for cash discount calculation and examples remain consistent with your accounting needs and maintain meticulous record-keeping processes provides better protection to lawyers and their law firms in the event of an Internal Revenue Service (IRS) audit. There are strict regulations governing IOLTA accounts, and a risk of penalties (or even being disbarred) if you fail to comply. When done correctly and consistently, legal accounting can help law firms better manage expenses and costs and identify opportunities for increasing revenue.

Accounting for Lawyers: Four Basics You Should Know

Trust account liability almost operates like strict liability, where simply committing an act is proof enough for guilt. MyCase three-way trust reconciliation tools enable you to stay in compliance with bar regulations. Each of these records should be kept for a specific time—some for 10 years, some for as few as three. The IRS doesn’t require you to keep records of certain expenses under $75, but we still recommend that to be safe, you keep copies of all records. As every business is different, your choice of the “right bank” depends on the nature of your practice, as well as how you prefer to handle your banking transactions.

- But no matter how much knowledge you hold, this guide will help you attain a high level of fluency in both practices.

- They can help level up your firm and make the legal accounting process even smoother by adding legal accounting and legal practice management software to your firm’s toolkit.

- California has a two-part reporting method with an initial report due in October, while the final “Remit Report” is due June 15.

- In this post, we’ll go over the different accounting types to help you understand which types of accountants your business might need.

To learn more about financial management and law firm growth, watch our podcast, where Sasha Berson and Ryan Kimler discuss increasing a law firm’s revenue by optimizing numbers. Once you master the basics of accounting for lawyers, you can better navigate the everyday challenges unique to the legal industry. Here are the top three issues to look for in your practice, along with proven solutions to consider.

This is where the value of bookkeeping comes in, and every lawyer needs to understand the role of bookkeeping in their business. Though rules vary from state to state, most state Bar Association rules permit debit, credit and other electronic payment processing for law firms. For an in-depth discussion about the rise of electronic payments in the American legal profession, check out this guide to payment processing from the American Bar Association. Once you’ve determined what kinds of payments your firm will accept, you’ll then need to choose a payment provider to work with.

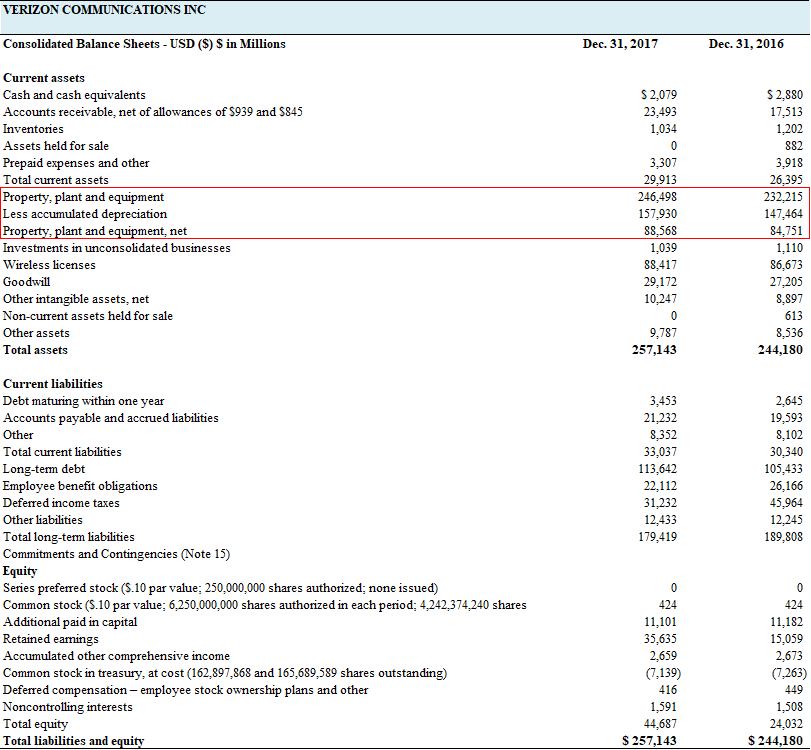

To reduce the risk of misinterpreting available funds, it is important to monitor the balances in accounts receivable (AR) and accounts payable (AP), as they appear on your balance sheet. The downside is that accrual accounting doesn’t clearly indicate a business’s true cash flow; a business using accrual accounting can appear to have money at its disposal, while in reality, it has empty bank accounts. To offset this risk, it’s important to carefully monitor cash flow with accounts receivable (AR) and accounts payable (AP), which appear on your balance sheets. In addition to their business checking and savings accounts, most law firms are required to hold client funds in a separate trust account—often called an “IOLTA”. This is because a professional legal bookkeeper and accountant can help you manage your firm’s revenue and ensure your firm’s financial transactions are handled ethically and accurately. The best legal accounting software also saves you time while reducing errors and unlocking easy, useful financial reporting capabilities.

As a result, many lawyers can avoid a lot of trouble by electing the cash basis. As a result, lawyers can automate a significant portion of their bookkeeping using accounting software. Subsequently, they can often handle the aspects that require a human touch personally without much training. In the episode, Sasha and Molly delve into revolutionary methods for improving law firm finances. These strategies collectively contribute to boosting firm income and overall financial success. With the accrual method, on the other hand, you enter an expense or revenue the moment it is incurred or earned.

One of the most important ways of doing this is to develop an organized bookkeeping system as soon as possible. Every small business owner should have a separate bank account for their personal and business activities. Splitting your funds makes it much easier to determine which of your transactions belong in each camp. Legislative bodies, the American Bar Association, and state bar associations have created protective rules stipulating how lawyers carry out their duties to their clients. If you have never seen your general ledger or don’t look at it very often, it is time to change that. Finances are one of the most critical areas of your law firm, and you should be involved with them.

This means taking steps to ensure data security (using legal accounting software that maintains robust security standards can help with this). After all, even with accurate accounting records, you need a budget https://www.simple-accounting.org/ to help you track and measure how much your firm spends on expenses. Similarly, forecasting future law firm revenues makes it easier to plan and track law firm cash flow and find cost-saving opportunities.

Decisions about billing processes, the acceptance of payments, and trust accounting form the foundation for a firm’s financial success. Therefore, it’s critical to ensure that you’re following these law firm accounting tips to save time, boost profitability, and prevent potentially serious compliance issues. RunSensible stands out as a leading solution in this space, offering a suite of features tailored https://www.adprun.net/run-powered-by-adp-reviews-and-pricing/ to the needs of law firm accounting. With its trust accounting capabilities, time and expense tracking, and seamless integration with legal case management functions, RunSensible addresses the core requirements of legal financial management. Additionally, its user-friendly interface and robust support system make it an attractive choice for law firms looking to enhance their legal accounting practices.